POPULAR ARTICLES

- Top E-Invoicing Service Providers in UAE: FTA Approved List

- UAE e-Invoicing Frequently Asked Questions (FAQs)

- How to Choose Your UAE E-Invoicing Technology Partner

- SAP UAE E-Invoicing Integration for SAP S/4HANA, ECC & SAP Business One

- List of ERP Changes Required for UAE E-Invoicing Compliance

- AP e-Invoicing in UAE: How Buyers Receive and Process E-Invoices?

- API, Middleware & ERP Integration for UAE E-Invoicing

RELATED ARTICLES

- e-Invoicing in UAE: Key Requirements, Implementation Timeline & Latest Updates

- What is the Peppol CTC Model in UAE for E-Invoicing?

- UAE e-Invoicing Frequently Asked Questions (FAQs)

- UAE Tax Credit Note: Examples, Formats & Benefits

- Digital Signature Certificate in UAE: Benefits, Process & How It Works

- VAT Invoice in UAE: Mandatory Details & Format

- VAT Rate List in UAE

- How to Claim VAT Refund in UAE?

- What are the Penalties for Non-Compliance under the UAE VAT?

- TRN Verification in UAE: Step-by-Step Process to Verify VAT Number in UAE

- Excise Registration in UAE: A Comprehensive Guide

YOU MIGHT BE INTERESTED IN

e-Invoicing UAE: Key Requirements, Implementation Timeline & Latest Updates

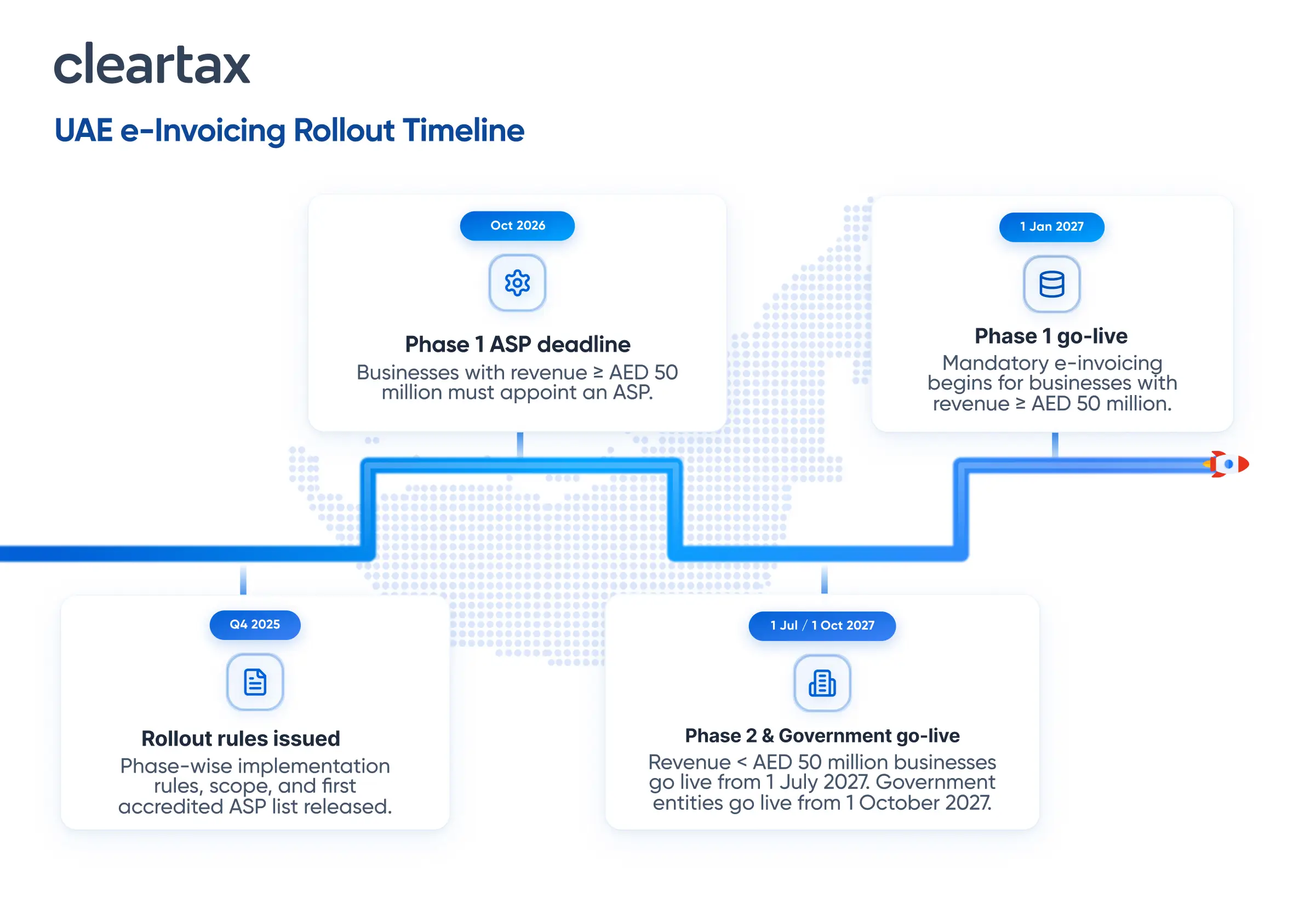

e-Invoicing UAE under the Electronic Invoicing System (EIS UAE) becomes mandatory from January 2027. Businesses handling B2B or B2G transactions in the UAE, whether, VAT registered or not will need to issue invoices in structured XML format, then send them through an Accredited Service Provider (ASP), to be chosen by 30 October 2026.

Key Takeaways

- Mandatory for all UAE businesses and government entities in scope for B2B/B2G and G2B transactions, whether VAT-registered or not, including free zone businesses unless specifically excluded.

- Phase 1 deadline: 1 January 2027 for businesses with revenue of AED 50 million or more; these businesses must appoint an ASP by 30 October 2026.

- Only structured XML invoices transmitted through an ASP qualify as valid e-invoices under the UAE framework. PDFs and paper invoices not valid.

- Non-compliance can trigger penalties of up to AED 5,000 per month for certain violations, making early readiness essential for e-invoice UAE 2027.

What is e-Invoicing in UAE?

E-invoicing in the UAE refers to the electronic creation, exchange, and storage of invoices in a structured digital format under the government’s new Electronic Invoicing System (EIS). This move is part of the UAE’s wider strategy to digitize tax administration, enhance VAT compliance, and align with international best practices.

Traditional PDFs or scanned invoices won’t qualify anymore. A valid UAE e-invoice must:

- Be issued in structured formats like XML using standards such as Peppol PINT-AE.

- Be transmitted through an Accredited Service Provider under the Peppol-based DCTCE model, sometimes called the 5-corner model.

- Be exchanged through ASPs while required Tax Data gets reported to the FTA with electronic confirmations for compliance monitoring.

UAE e-Invoicing Implementation Timeline (2026–2027)

The UAE government released updated regulations through Ministerial Decision No. 243 of 2025 plus Ministerial Decision No. 244 of 2025 on 28 September 2025, also highlighted by the 1 June 2026 dated Version 1.1 of the Electronic Invoicing Guidelines released by the UAE MoF. These decisions formally set out the phased rollout of the Electronic Invoicing System.

10th May 2026 MoF update: The Ministry of Finance extended the ASP appointment deadline for businesses with revenue of AED 50 million or more. Earlier it was 31 July 2026. Now it is 30 October 2026. Yet the mandatory go-live date still remains 1 January 2027.

Types of Electronic Invoices Can Be Issued

The UAE e-invoicing framework covers different electronic document types depending on the transaction, VAT treatment and billing arrangement. The key types include:

- Electronic Tax Invoice: Used for taxable supplies requiring a VAT Tax Invoice under UAE VAT law.

- Electronic Tax Credit Note: Issued when correcting, reducing, or cancelling an earlier Electronic Tax Invoice.

- Commercial Invoice: Used for exempt supplies, out-of-scope transactions, or non-VAT transactions where VAT invoices are not required.

- Electronic Credit Note: Adjusts or reverses Commercial Invoices or other non-tax invoice scenarios.

- Self-billed Electronic Tax Invoice: Issued by the buyer on behalf of the supplier where self-billing is allowed plus contractually agreed.

- Self-billed Electronic Tax Credit Note: Buyer-issued correction document for self-billed invoices.

UAE e-Invoicing Requirements: What Your Invoice Must Meet

A UAE digital tax invoice is not simply a PDF exported from an ERP system. It must be a structured XML format invoice exchanged through an ASP.

To comply with the UAE e-invoicing system, businesses need to meet these requirements:

- Invoices must exist only in digital structured formats like XML. PDFs or paper copies don’t count.

- Recognized standards such as PINT-AE or UBL must be used.

- Invoices must move through an Accredited Service Provider approved by the Ministry of Finance.

- Invoices plus credit notes need to be transmitted according to timelines prescribed under the Electronic Invoicing System.

- Mandatory invoice fields, seller details, VAT number, tax breakdown, others, must follow the official Data Dictionary.

- Credit notes must also be electronic.

- Invoice data must be stored securely in a way that preserves integrity and allows retrieval by the FTA under the Tax Procedures Law.

- Advance and final invoice linking Rulebook v1.1 (1 June 2026) makes linking the advance and final invoices mandatory: enter the advance in the 'Paid Amount' field and cite the advance invoice in the 'Preceding Invoice Reference' field.

- Retention billing Rulebook v1.1 (1 June 2026) also updates retention billing in contracting and real estate: the e-invoice must show only the net amount payable at that event, with VAT on that net figure, and a separate tax invoice with VAT is issued later when the retained amount is released.

Mandatory Fields of an e-Invoice in the UAE

Every e-invoice and e-credit note must include all data fields and particulars prescribed by the Ministry of Finance. These fields follow the UAE e-Invoicing Data Dictionary and align with Peppol/UBL standards.

Category | Mandatory Fields |

Seller (Supplier) Information | Legal name of supplier Address and contact information ASP identifier or system ID |

Buyer (Recipient) Information | Legal name of buyer TRN (if VAT registered) Address and contact details |

Invoice Metadata | Unique Invoice Number (Electronic Invoice sequential number + UUID) Issue Date and Time (in UTC) Invoice Type Code (standard, credit note, or debit note) Currency Code (AED or applicable foreign currency) |

Transaction Details | Description of goods or services Quantity and unit of measure Unit price and total before tax VAT rate and VAT amount per line item Discounts or adjustments (if applicable) |

Tax Summary | Total taxable amount Total VAT amount Gross invoice total (inclusive of VAT) |

Digital and Transmission Details | ASP digital signature and validation stamp Reference to previous invoice (for credit/debit notes) Transmission timestamp and system acknowledgment ID |

Optional / Additional Fields | Purchase order reference number Payment terms and due date Bank details or IBAN Remarks for buyer or FTA audit trail |

How UAE e-Invoicing Works: Step-by-Step Process

To comply with the UAE’s e-Invoicing mandate, businesses will need to follow a structured process supported by their ERP systems and Accredited Service Providers (ASPs). Here’s how it works in practice:

- Hire an Accredited Service Provider (ASP): Businesses must appoint an FTA accredited ASP. The ASP works with your technical/ERP team to customize your ERP so that it can capture all relevant invoice data fields required by the FTA (often called the “data dictionary”).

- Map ERP Data to Standard Fields: Each e-invoice requires specific information such as seller/buyer details, VAT registration number, item description, taxable amount, VAT rate, total invoice value, etc. The ASP ensures your ERP is aligned with this data dictionary and maps the captured fields correctly. You must also capture the buyer’s Participant Identifier (End Point ID) where available (0235 + 10-digit TIN).

- Convert to Required Format: After putting invoice details into the ERP system, the ASP changes the invoice into the special digital format called XML. It uses approved formats like UBL or Peppol PINT-AE.

- Validate and Enrich: Before sending the invoice, the ASP checks all the details carefully, fixes mistakes if there are any, plus adds missing important details like special codes or ID numbers so the invoice follows the rules properly.

- Real-Time Transmission: The ASP then sends the invoice at the same time to:

- The FTA’s e-Billing system, for monitoring and compliance. (Tax Data reporting with electronic confirmation)

- The buyer’s ASP, so the recipient receives the invoice in a processable format. If the buyer is not yet onboarded and does not have a Participant Identifier, the supplier must use the predefined endpoint (0235:9900000098); for deemed supply use (0235:9900000097); and for exports where the buyer has no Peppol ID use (0235:9900000099).

- Secure Storage and Access: Both the sender plus receiver must keep the e-invoice and related details stored safely. The information should stay complete, protected, plus easy for the FTA to find later when needed. e-invoicing guidelines version 1.1 released on 1 June 2026 further allows offshore/cloud hosting of data, provided it is retrievable by the FTA.

UAE e-Invoicing Framework: The DCTCE (5-Corner) Model

The UAE’s CTC e-invoicing framework, known as the "DCTCE" model, is based on the Peppol "5-corner" model. The "5-corner" model involves five main components:

- Issuer: The party generating the invoice.

- Receiver: The party receiving the invoice.

- E-Billing System by FTA: Integrates with the Peppol PINT (Peppol Invoice Standard) for data exchange. The e-billing platform acts as an invoice repository but does not validate the invoices.

- Sender Accredited Service Provider (ASP): Verifies the data and transmits the invoice to the tax authority and the receiver ASP

- Receiver ASP: Verify the received data and transmit the e-invoice to the purchase party (receiver)

Scope of e-Invoicing in UAE

The scope of e-invoicing in the UAE is defined under Ministerial Decisions No. 243 and 244 of 2025. Further, UAE Electronic Invoicing Guidelines, Version V 1.1, released on 1 June 2026 provides new rules for how to show advance payments and retention amounts in e-invoice (money held back until a job is finished). The Electronic Invoicing System applies broadly to most business transactions carried out in the UAE, with certain exclusions and phased implementation requirements.

- All persons conducting business in the UAE may fall under the requirement to issue and exchange electronic invoices or credit notes through the system, regardless of VAT registration status.

- Both B2B plus B2G transactions are covered.

e-Invoicing Exemptions in UAE

Certain categories of transactions are excluded from mandatory e-invoicing under Article 4 of Ministerial Decision No. 243/2025:

- B2C transactions are not subject to mandatory e-invoicing

- Transactions conducted by government entities in a sovereign capacity that are not in competition with the private sector.

- International passenger air transport services where electronic tickets are issued.

- Ancillary airline services linked to passenger transport when an Electronic Miscellaneous Document (EMD) is issued.

- International transport of goods by air, where an airway bill is issued. This exclusion applies for a limited period of 24 months from the system’s effective date.

- Financial services that are VAT-exempt or zero-rated.

- Any other transactions determined by the Minister of Finance.

Role of Accredited Service Providers (ASPs) in UAE e-Invoicing

As per UAE regulations, all taxpayers subject to the e-invoicing mandate must appoint an Accredited Service Provider (ASP) prior to implementation deadlines (July 2026: January/October 2027, depending on revenue and entity type). This requirement reflects the UAE’s decision to adopt a Peppol-based Continuous Transaction Control (CTC) model, where ASPs are central to ensuring compliance, accuracy, and secure transmission of e-invoices.

Key Functions of ASPs in UAE e-Invoicing

- Data Mapping: Align invoice data from the business ERP and accounting systems with the structured formats the FTA requires. Use XML through UBL or PINT-AE so the data moves cleanly and without confusion.

- Validation: Check each invoice against the UAE e-invoicing schema, the VAT law, and the Peppol standards before it is sent. Errors caught early save time later.

- Data Enrichment: Add missing details like digital signatures, tax information, or special ID numbers so the invoice follows all rules properly.

- Format Conversion & Correction: Convert invoices from PDF, CSV, or Excel into computer-friendly formats the system accepts. Fix mistakes before sending so the invoice does not fail in transit.

- Transmission: Route invoices securely through the Peppol network to the Federal Tax Authority (FTA) and the recipient ASP in real time. The process must move fast and stay secure.

- Compliance Reporting: Make sure invoices and credit notes reach the FTA within the correct time limit, including the 14-day reporting period where needed.

- Security & Authenticity: Protect invoice data using digital signatures, encryption, plus safety tools so nobody changes or damages the information.

- Integration Support: Help ERP systems plus business software connect smoothly using APIs, middleware, and onboarding support.

- Monitoring & Notifications: Watch invoice status in real time, send alerts if something fails, plus keep backup steps ready during system problems.

- Archival & Storage: Store e-invoices plus related records safely for the time required under UAE rules.

UAE e-Invoicing Penalties and Fines

The UAE Ministry of Finance has issued Cabinet Decision No. 106 of 2025, which defines administrative penalties for non-compliance with the UAE Electronic Invoicing System. These penalties apply to issuers and recipients once they are formally mandated to adopt e-invoicing. Businesses using e-invoicing voluntarily before being mandated are not subject to these fines.

Violation | Who it applies to | Penalty amount | How it’s calculated / cap |

Failure to implement e-invoicing or appoint an Accredited Service Provider (ASP) within the prescribed timeline | Issuer | AED 5,000 | For each month or part of a month of delay |

Failure to issue and transmit an electronic invoice through the system on time | Issuer | AED 100 per invoice | Capped at AED 5,000 per calendar month |

Failure to issue and transmit an electronic credit note through the system on time | Issuer | AED 100 per credit note | Capped at AED 5,000 per calendar month |

Failure to notify the Authority of a system failure within the prescribed timeline | Issuer | AED 1,000 per day | For each day (or part of a day) of delay |

Failure to notify the Authority of a system failure within the prescribed timeline | Recipient | AED 1,000 per day | For each day (or part of a day) of delay |

Failure to inform the appointed ASP of updates to Authority-registered data within the prescribed timeline | Issuer or Recipient | AED 1,000 per day | For each day (or part of a day) of delay |

How to Prepare for e-Invoicing (Effective July 2026)

Businesses getting ready for e-invoice UAE 2027 should start early. This helps finish ERP changes, ASP setup, and testing before the deadline comes:

1. Understand the Timeline and Scope: The pilot phase begins in July 2026. Then there will be phased enforcement based on business size. Big businesses earning AED 50 million or more must follow the rules first. Smaller businesses plus government bodies follow later, even if they are not VAT-registered. Businesses doing only B2C sales do not need to follow these rules right now.

2. Appoint an Accredited Service Provider (ASP): All persons conducting Business in the UAE must appoint an FTA-approved ASP before implementation. For businesses searching for the FTA e-invoicing portal, onboarding with the chosen ASP begins in EmaraTax through the FTA website. Complete onboarding before your phase deadline and ensure the ASP follows Peppol standards like UBL or PINT-AE.

3. Upgrade ERP and Accounting Systems: ERP systems must create structured invoices in XML, map all fields to the Ministry’s data dictionary, apply digital signatures, and link directly to the ASP. Manual or PDF invoices will no longer qualify as valid once e-invoicing takes effect.

4. Test During the Pilot Phase: Businesses should test the system during the pilot phase from July to December 2026. Check if the ERP, ASP, and FTA systems work correctly together. Test sample invoices, check data properly, and train employees to use the new process.

5. Establish Data Governance and Storage: Keep e-invoices, credit notes, and related records stored safely according to UAE tax rules. The information should stay complete, protected, and easy for the FTA to find later if needed.

6. Ensure Compliance and Reporting Readiness: Update VAT workflows for real-time reporting. Make protocols for handling technical problems. If any system stops working, inform the FTA within 2 business days. Train employees properly. Be financially ready for ASP setup, digital signatures, plus compliance work.

How ClearTax Can Help Your Business with e-Invoicing in UAE?

ClearTax is a fully approved FTA and MoF-compliant Accredited Service Provider (ASP) that can help your business comply with the UAE’s e-invoicing requirements. ClearTax offers a Peppol-ready solution that seamlessly integrates your business system with the FTA portal, ensuring secure and compliant transmission of invoice data.

Here’s how ClearTax can assist:

- Integration with the FTA Portal: ClearTax integrates your business system with the FTA’s e-billing system, ensuring that e-invoices are submitted in real-time, using the specified formats like XML.

- Peppol-Ready: ClearTax follows the Peppol specifications for data exchange, ensuring compliance with the UAE’s Continuous Transaction Controls (CTC) model.

- End-to-End E-Invoicing Solution: ClearTax provides a complete solution for issuing, submitting, and receiving e-invoices. It tracks the status of submitted invoices sends email notification for e-invoices.

- Web-Based Portal: ClearTax gives an easy online portal where businesses can create invoices, submit them, plus track their status in one place.

- 100% E-Invoicing Compliance: ClearTax helps businesses follow UAE e-invoicing rules completely.

Frequently Asked Questions

About the Author

Rajan Rauniyar

I’m a Senior Content Writer at ClearTax, specializing in e-invoicing, VAT, and Tax compliance. Over the years, I’ve researched and written everything from blog posts to whitepapers and product guides, helping ClearTax expand in Malaysia, KSA, UAE, Singapore, Belgium, France and beyond. My goal is to write the most comprehensive, understandable, readable, and accurate content on any topic that has ever existed on the internet. Read more

Your data security and privacy matter most to us.